Fixed income investing can offer a number of benefits, such as providing a predictable source of income, helping to preserve capital and offering attractive diversification benefits to your portfolio.

What is a bond?

A bond is a financial instrument that allows a government or corporation to borrow money from investors. It is typically issued at a set rate of interest over a specific period of time – from the date the bond is issued to its maturity date. The interest rate (or coupon) that is paid for this loan is determined by a variety of factors, such as the creditworthiness of the issuer and the prevailing rate of interest offered in the market at that point in time.

Bonds issued by governments typically pay a lower rate of interest than corporations because there is a lower risk that they will be unable to pay back the loan.

Provided you buy a bond for the same price as its principal value, your investment return will be the value of the coupon payments you received, assuming the original amount is returned to you in full. If you decide to sell your bond in the market prior to its maturity date you may also have a gain or loss based on whether the bond was worth more or less than the principal value.

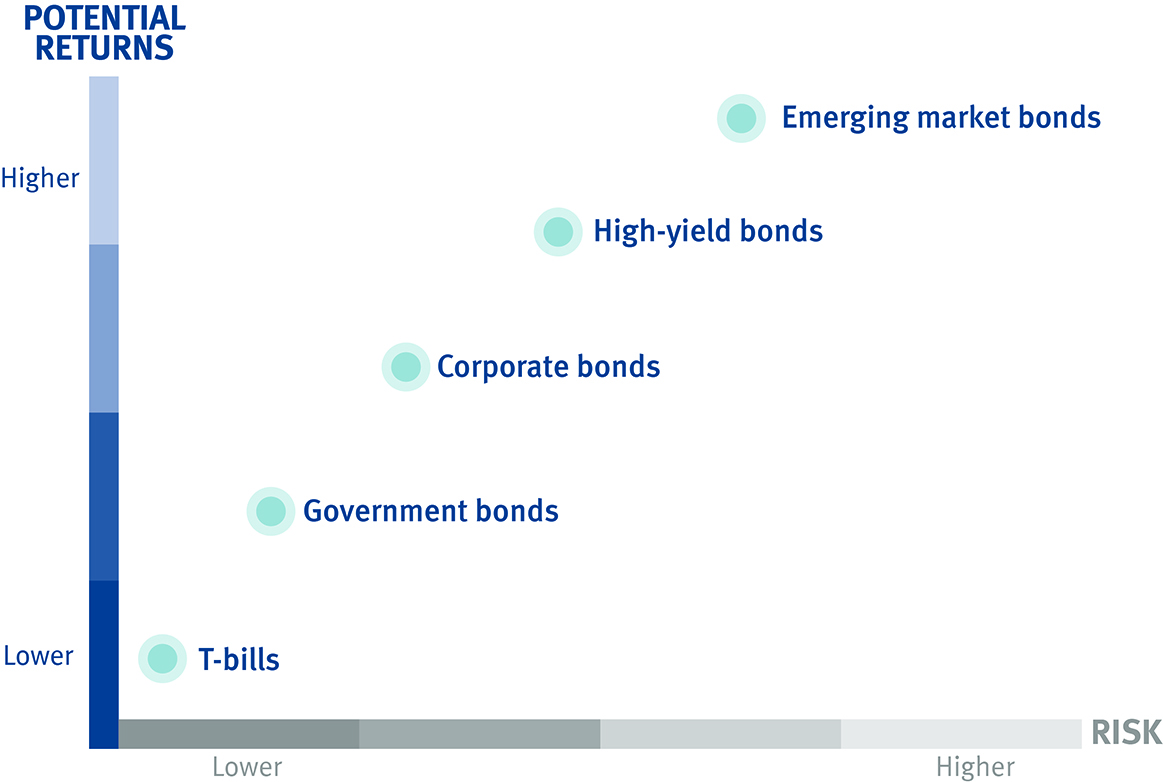

The different segments of the bond market

Fixed income investments are not all created equal, and therefore it is important to hold a diversified mix of fixed income investments in your portfolio. Each segment, however, reacts differently to changes in interest rates, the economic outlook and other market factors.

This chart generally illustrates the various risk and potential return levels for T-Bills and a variety of bond segments.

Today's fixed income markets have changed dramatically over the last 10 years. Investors have more options than ever. Though there is a lot of talk about rising rates today, yields are still low compared to long-term norms. But there are opportunities out there for active investors to boost yields by diversifying their fixed income holdings.

In these short video clips, you'll hear from Dan Chornous, RBC GAM's Chief Investment Officer, and Dagmara Fijalkowski, Head, Global Fixed Income & Currencies on some of the questions most frequently asked about fixed income.

Skip directly to a topic by clicking on a link below:

Think of yield as the return provided by a fixed income investment. The yield of a bond is based on both the purchase price of the bond and the interest (or coupon) payments received each year. Yield is often the term used to describe long-term interest rates.

Yield = Coupon

Bond Purchase Price

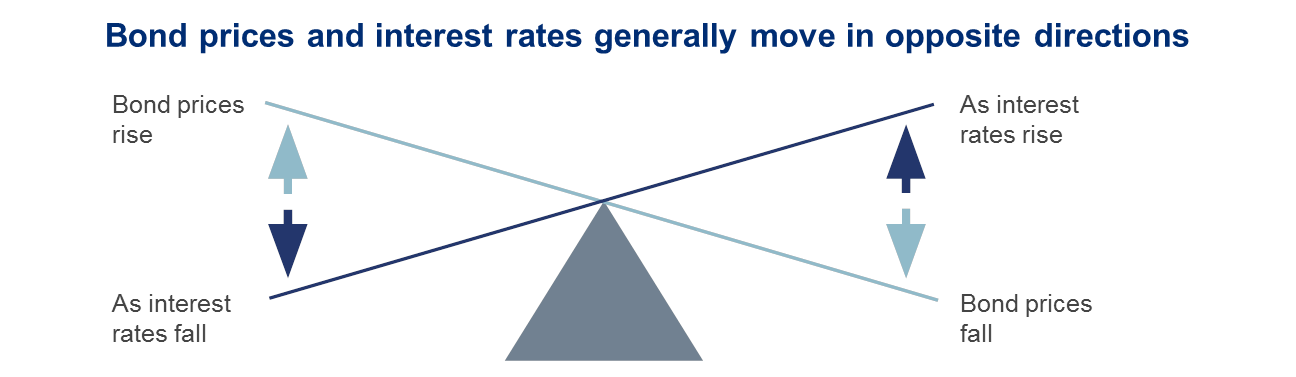

Why Rising Interest Rates (and Yields) Push Down Bond Prices

Interest rates and bond prices have an inverse relationship. When interest rates fall, bond prices usually rise and when interest rates rise, bond prices usually fall.

Example

An investor buys a new bond for $1,000 that has a 6% interest payment (yield) earning $60 in interest each year. (This interest payment is generally referred to as a coupon.) If interest rates increase by 1%, new bonds will provide a 7% interest payment, paying investors $70 annually. Because investors will now be able to buy a bond with a higher interest payment (higher yield), not as many people will want to buy the 6% bonds. This decline in demand will cause the value of the 6% bond to fall.

The key point is that a bond’s yield will rise when the value of the bond declines. So when bond yields (or interest rates) rise, it actually means that the value of bonds in general is declining. This is why rising bond yields are generally considered to be undesirable for existing bond investors.

Talk to your advisor about how changing interest rates may impact your portfolio. Your advisor can help you determine appropriate investment solutions for your portfolio in the current environment.

Money Market Securities

T-Bills, Commercial Paper and Bankers’ Acceptances

Treasury bills (T-Bills) and other money market securities such as commercial paper and bankers’ acceptances are considered to be the safest segment of the fixed income market.

Issued at a discount, T-Bills are short-term debt securities issued or guaranteed by federal, provincial or other governments. The stated interest rates for T-Bills are fixed when issued, but values fluctuate based on changes to the central bank rate. A T-Bill’s return is calculated based on the difference between the price paid and the par value (also known as the denomination or face value). T-Bills mature at par (typically 90 or 180 days) and do not pay fixed interest payments like most bonds.

Unlike T-Bills, commercial paper and bankers’ acceptances are issued by corporations. A commercial paper is a negotiable promissory note with a term of a few days to a year and is not generally secured by company assets. A bankers’ acceptance is a short-term promissory note bearing the unconditional guarantee (acceptance) of a major chartered bank. Bankers’ acceptances offer superior yields to T-Bills, with higher quality and liquidity than most commercial paper issues.

To learn about the funds we offer that invest primarily in T-bills and other money market securities, see:

Government Bonds

Issued with terms to maturity between 2 and 30 years, government bonds are considered very low-risk fixed income investments as they are backed by governments. The value of government bonds fluctuates based on supply and demand in the market – a government will increase the supply of bonds to raise money, which will be used to stimulate the economy.

Demand for government bonds tends to increase during periods of low confidence in equity markets as investors seek safety. Demand also tends to increase in periods of weak economic activity when the threat of inflation is minimized.

To learn about the funds we offer that invest primarily in government bonds, see:

Corporate Bonds

Investment-Grade Corporate Bonds

Issued by large corporations, these corporate bonds are often called “investment grade” because they are issued by very creditworthy companies with high credit ratings. Standard & Poor’s assigns credit ratings of AAA, AA, A or BBB to investment-grade bonds.

Investment-grade corporate bonds offer a slightly higher stream of income than government bonds because they are not guaranteed by a government. The difference in rates (interest-rate spread) between corporate and government bonds generally rises and falls as a result of investor confidence, investors’ willingness to take risks, the outlook for the economy and growth in corporate profits. (Interest-rate spread – or simply spread – is used to describe the difference in rates between different types of bonds.)

With investment-grade corporate bonds, investors assume the risk that the issuing company might not be able to make its interest and principal payments. The risk of investment-grade corporate bonds, however, tends to be very low.

To learn about the funds we offer that invest in investment-grade corporate bonds, see:

High-Yield Corporate Bonds

High-yield corporate bonds are sold by corporations that do not have the same high credit rating as investment-grade issuers. Standard & Poor’s assigns credit ratings of BB or lower to high-yield bonds.

Historically, high-yield bonds have provided investors with a higher yield than investment-grade corporate or government bonds. This higher yield helps to compensate investors for the risk of the issuing company not making its interest and principal payments.

Due to their higher risk of default, the interest-rate spread between high-yield bonds and government bonds is wider than the spread between investment-grade corporate bonds and government bonds.

To learn about the funds we offer that invest in high-yield corporate bonds, see:

Emerging Market Bonds

Emerging market bonds are issued by governments or companies in developing countries. Emerging market bonds typically pay higher yields than investment-grade bonds in both Canada and the U.S. This extra yield pays investors for the added risk of investing in countries with shorter records of sound economic policies and less established institutional and governmental frameworks.

In recent years, many emerging market countries have adopted conservative banking and regulatory regimes – similar to those in Canada – which have reduced the risk and increased the credit quality of their bonds.

To learn more about funds we offer that invest in emerging market bonds, see: