RBC Target Maturity Corporate Bond ETFs represent a family of fixed income ETFs maturing in successive years ranging from 2017 to 2023. Each ETF tracks a unique FTSE TMX Maturity Canada Corporate Bond Index™ that maintains a portfolio of Canadian investment grade corporate bonds structured to mature in the same year as the ETF itself and is monitored by FTSE TMX Debt Capital Markets Inc.

For investors, the RBC Target Maturity Corporate Bond ETF is intended to be a replacement for holding individual corporate bonds. They help the fixed income portion of an investment portfolio to:

- Reduce risk through issuer diversification

- Enhance returns through institutional bond pricing, transparency and greater liquidity

Recognized as funds that deliver consistently strong performance through an entire calendar year.

- RBC Target 2018 Corporate Bond Index ETF (RQF)

- RBC Target 2020 Corporate Bond Index ETF (RQH)

- RBC Target 2021 Corporate Bond Index ETF (RQI)

Additional Information

- RBC ETFs Product List

- ETF Investing: Tax Questions

- Understanding TMCB ETFs

- RQE FAQ

- Bond Basics

- Index tracking methodologies

Yield to Maturity Calculator

The Estimated Net Acquisition Yield Calculator provides an approximation of the yield to maturity an investor can expect.

Read more>Overview

RBC Target Maturity Corporate Bond ETFs

These ETFs are designed to provide investors with an investment solution that blends the diversification, and cash flow characteristics of a fixed income mutual fund, the maturity profile of an individual bond, and the intra-day trading characteristics of a stock.

| TSX Symbol | Target Maturity Corporate Bond ETFs | Monthly Update |

|---|---|---|

RQE |

RBC Target 2017 Corporate Bond Index ETF | |

RQF |

RBC Target 2018 Corporate Bond Index ETF | |

RQG |

RBC Target 2019 Corporate Bond Index ETF | |

RQH |

RBC Target 2020 Corporate Bond Index ETF | |

RQI |

RBC Target 2021 Corporate Bond Index ETF | |

RQJ |

RBC Target 2022 Corporate Bond Index ETF | |

RQK |

RBC Target 2023 Corporate Bond Index ETF |

Understanding Distributions

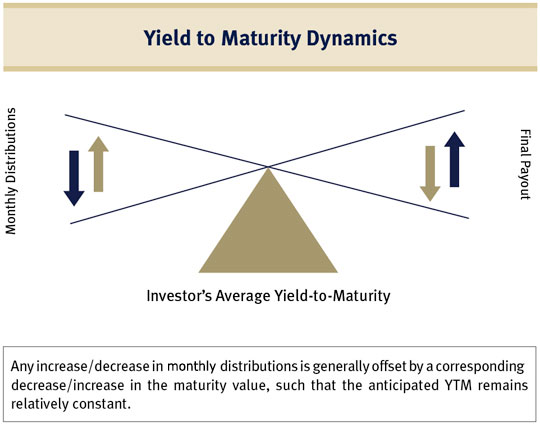

RBC Target Maturity Corporate Bond ETFs are an innovative solution in the landscape of the rapidly growing ETF market. A unique and important feature of the RBC TMCB ETF structure is that they are designed to allow investors to determine with a fair degree of accuracy their expected yield to maturity (YTM).

Having a known YTM allows an investor purchasing an RBC TMCB ETF to be confident in knowing their total expected annualized return from their date of purchase through to the ETF maturity date. While this is a feature similar to an individual bond, there are differences in the way cash flows are paid out between these two investment options. Individual bonds make regular fixed coupon payments and a fixed payment at maturity (the maturity or par value). RBC TMCB ETF payments are comprised of monthly distributions and a similar payout at maturity, but unlike with an individual bond these payments may fluctuate. This is due to:

- The differences in monthly distributions from a bond portfolio (e.g., ETFs) vs. fixed coupon payments from an individual bond.

- The addition of new issues to the index (and therefore tracked by the ETF).

- The methodology for winding down the ETF in the year of its maturity.

However, regardless of the cash flow adjustments, the investor will still receive the same average YTM (total annualized return) if the ETF is held to maturity. This is because of the unique proprietary conditional rebalancing process utilized by the RBC TMCB ETFs.

How to Use in Your Portfolio

RBC Target Maturity Corporate Bond ETFs target dated maturity structure facilitates the implementation of several fixed income strategies that previously had only been feasible through investing in individual corporate bonds.

Bond Laddering

A laddered bond portfolio is comprised of several fixed income holdings, each having a successively longer term to maturity. In a typical laddered portfolio, every position or holding in the portfolio would be the same size with an equal time interval between maturities. As bonds in a laddered portfolio mature, the cash distribution is either utilized to cover lifestyle needs or reinvested in new bonds at the longest maturity of the ladder at the then current market interest rate.

While a bond laddering strategy can help mitigate interest rate risk, investors who utilize individual corporate bonds remain exposed to several other risk factors. These risks include credit risks associated with holding individual corporate issuers, price transparency in the over the counter (OTC) corporate bond market, and liquidity risks. Utilizing the RBC Target Maturity Corporate Bond ETFs may help mitigate some of these risks due to the design and investment mandate of the product.

Filling the gap in existing laddered portfolios

For investors with existing laddered bond portfolios, the RBC Target Maturity Corporate Bond ETFs can be effective for filling gaps in the ladder. Due to the mechanics of the corporate bond market it may be difficult for investors to find a suitable corporate bond that fulfills the desired maturity profile when required. As the RBC Target Maturity Corporate Bond ETF is traded on the exchange, investors are provided with an easily accessible product to replace an individual corporate bond.

Targeted exposure

Certain investors may believe that parts of the corporate yield curve are cheap or expensive. Acting upon this view can be difficult using individual corporate bonds. In order for an investor to initiate this trade several conditions must first be in place. There must be product available at the particular part of the curve for which the investor desires exposure. Providing the investor can find an appropriate corporate bond that satisfies the first condition, they must also be cognizant of the issuer’s credit rating and credit outlook. In other words, the investor’s belief that a certain part of the corporate yield curve is inexpensive may be correct, but if the investor gains such exposure by investing in an issuer whose bond declines in price due to credit deterioration, they may not fully realize all of their expected returns. Since the RBC Target Maturity Corporate Bond ETF invests in a basket of corporate issues, the diversified portfolio limits the impact of credit deterioration of a single issuer.

What Happens at Maturity

The structure of an RBC Target Maturity Corporate Bond ETF is designed to provide a yield to maturity comparable to what an investor could realize if they were to hold to maturity a portfolio of Canadian corporate bonds of similar credit quality and maturity as those held by the fund. However, unlike an investment in an individual bond where investors typically receive the bond’s par (or face) value at maturity, the RBC Target Maturity Corporate Bond ETFs will distribute the fund’s net asset value (NAV) at maturity. The funds do not seek to return any predetermined amount at maturity, and the amount an investor receives may be worth more or less than their original investment.

Each of the target maturity ETFs will mature on or about November 30th of the stated maturity year. In the last year of operation, as the corporate bonds held by the fund mature, the portfolio will begin to invest the matured proceeds in cash and cash equivalents. These cash and cash equivalent investments include, but are not limited to, Government of Canada Treasury Bills and investment grade commercial paper. Consequently as the ETF nears maturity, and similar to a maturing bond, the fund’s yield to maturity profile will more closely reflect prevailing money market yields.

On the maturity date the fund will make a final cash distribution which will be comprised of:

- Any net income and/or net realized capital gains not previously distributed to unit holders.

- The remaining net assets (after making the appropriate provisions for any remaining liabilities) of the fund.

Even though investors receive the fund’s net asset value at maturity it is important to be aware of the fund’s par (face) value/unit. This figure represents the amount of principal (or par value) per unit held by the fund. When compared to the fund’s net asset value, investors will be able to determine if the fund is trading at a premium/discount to par. Much like an investment in an individual Canadian Corporate Bond, as the RBC Target Maturity Corporate Bond ETF approaches maturity, the difference between the net asset value/unit (NAV) of the fund and the par (face) value/unit will begin to narrow. To see how these characteristics of the fund compare to those of individual corporate bonds we have provided a quote for an individual Canadian Corporate Bond and the corresponding characteristics and likely values for the RBC Target Maturity Corporate Bond ETF.

Corporate Bond Quote vs. RBC Target Maturity Corporate Bond ETF

Corporate Bond

| Issue | Coupon | Effective Maturity |

Price | Yield to Maturity |

Par (Face) Value |

|---|---|---|---|---|---|

| Toronto Hydro Corp. | 3.54% | 2021 Nov. 18 | $109.18 | 1.82% | $100 |

RBC Target Maturity Corporate Bond ETF

| Issue | Weighted Avg. Coupon | Effective Maturity |

Net Asset Value / Unit |

Weighted Avg. Yield to Maturity |

Par (Face) Value / Unit |

|---|---|---|---|---|---|

| RBC Target 2021 Corporate Bond Index ETF | 3.83% | 2021 Nov. 30 | $20.33 | 2.28% | $18.71 |

The FundGrade A+ rating is used with permission from Fundata Canada Inc., all rights reserved. Fundata is a leading provider of market and investment funds data to the Canadian financial services industry and business media. The Fund-Grade A+ rating identifies Canadian investment funds that have consistently demonstrated the best risk-adjusted returns throughout an entire calendar year. For more information on the rating system, please visit www.Fundata.com/ProductsServices/FundGrade.aspx. FundGrade A+ is a supplemental calculation to the FundGrade ratings and is performed at the end of each calendar year. Eligible funds must have received a FundGrade rating every month in the previous year. FundGrade A+ uses a "GPA-style" calculation, where monthly FundGrades from "A" to "E" receive scores from 4 to 0, respectively (A FundGrade rating of A indicates a fund is in the top 10% of funds in its category). A fund's average score for the year determines its GPA. Any fund with a GPA of 3.5 or greater is awarded an A+ rating. A fund's FundGrade rating is subject to change monthly. The following were awarded the FundGrade A+ Award for the one-year period ending December 31, 2016: RBC 1-5 Year Laddered Corporate Bond ETF (RBO) and RBC Target 2018 Corporate Bond Index ETF (RQF)in the Canadian Short-Term Fixed Income category ( consisting of 134 other funds); RBC Target 2020 Corporate Bond Index ETF (RQH) and RBC Target 2021 Corporate Bond Index ETF (RQI) in the Canadian Fixed Income category (consisting of 358 other funds). Performance for the period ending April 30, 2017 is as follows: RBO 2.92 % (1 year), 2.53 % (3 years), n/a (5 years) and 2.70 % (since inception on January 15, 2014); RQF 1.98 % (1 year), 2.40 % (3 years), 3.24 % (5 years) and 3.38 % (since inception on September 15, 2011); RQH 3.00 % (1 year), 3.68 % (3 years), 3.89 % (5 years) and 4.34 % (since inception on September 15, 2011); RQI 3.69 % (1 year), 4.40 % (3 years), n/a (5 years) and 3.96 % (since inception on October 10, 2012).

*Source: RBC GAM as of March 31, 2016

FTSE TMX Maturity Canada Corporate Bond Indices™ are trademarks of TSX Inc., a subsidiary of TMX Group Inc., and have been licensed for use for certain purposes to RBC Global Asset Management Inc. by FTSE TMX Global Debt Capital Markets Inc. The RBC ETFs are not sponsored, endorsed, sold or promoted by FTSE TMX Global Debt Capital Markets Inc., FTSE International Limited, TMX Group Inc. or their affiliates, or third party data suppliers and they make no representation, warranty or condition regarding the advisability of investing in the RBC ETFs.

Commissions, management fees and expenses may be associated with investments in exchange-traded funds (ETFs). Please read the prospectus before investing. ETFs are not guaranteed, their values change frequently and past performance may not be repeated. ETF units are bought and sold at market price on a stock exchange and brokerage commissions will reduce returns. RBC ETFs do not seek to return any predetermined amount at maturity. RBC ETFs are managed by RBC Global Asset Management Inc., an indirect wholly-owned subsidiary of Royal Bank of Canada.